📊 Quick Summary

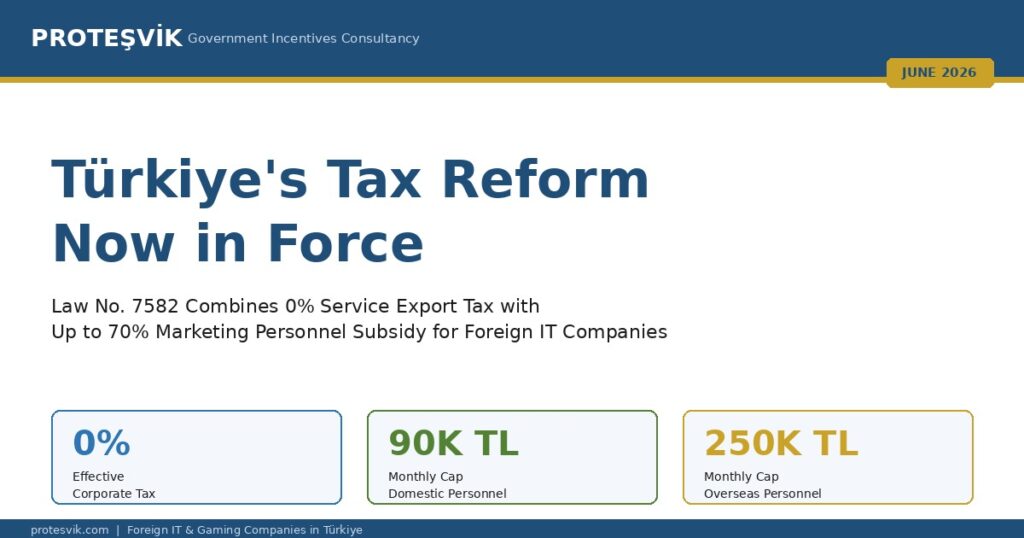

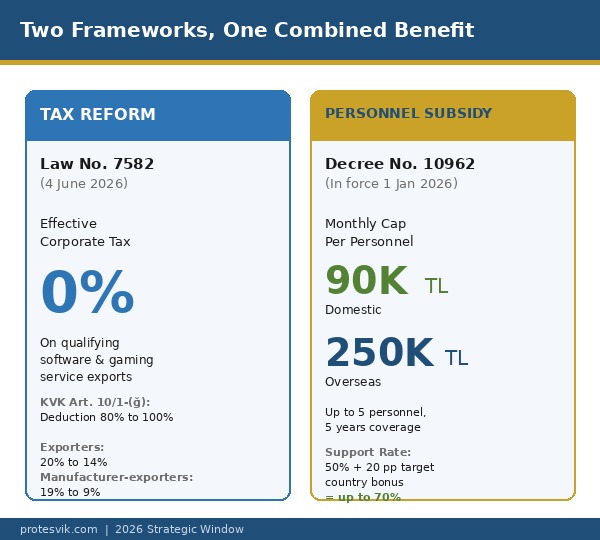

- New law in force: Law No. 7582 — published 4 June 2026, Official Gazette No. 33270

- Effective corporate tax on service exports: 0% (KVK Article 10/1-(ğ), deduction raised 80% → 100%)

- Headline corporate tax for exporters: 20% → 14%; for manufacturer-exporters 19% → 9%

- Personnel subsidy: up to 90,000 TL/month per domestic, 250,000 TL/month per overseas marketing personnel

- Subsidy rate: 50% standard, up to 70% with target country bonus, 5 personnel cap, 5 years

- Legal anchor: Presidential Decree No. 10962 (in force from 1 January 2026)

- Beneficiary structure: Türkiye-headquartered LLC, 100% foreign ownership permitted

- Setup time: 1–2 weeks; minimum capital 50,000 TL (~USD 1,110)

- Proteşvik service: Complimentary 30-minute feasibility assessment

The Türkiye tax reform — formally Law No. 7582 — is now in force as of 4 June 2026, marking a structural shift for foreign IT and gaming companies evaluating the country. Combined with the personnel subsidy framework already operating under Presidential Decree No. 10962, the two regulations create a structural cost advantage that founders and CFOs from China, India, Germany, South Korea, and the MENA region are increasingly building into their 2026 expansion roadmaps. This guide explains, with concrete figures and three illustrative scenarios, how the two frameworks work together in practice.

Türkiye Tax Reform Now in Force — Law No. 7582 (June 2026)

The Türkiye tax reform — formally the Türkiye Yüzyılı Tax Package — became law on 4 June 2026 when it was published in the Official Gazette under issue No. 33270 as Law No. 7582. The legislative timeline ran as follows:

- 24 April 2026: President Erdoğan announced the Türkiye Yüzyılı Investment Center Program from the Presidential Dolmabahçe Office

- 27 April 2026: Minister of Treasury and Finance Mehmet Şimşek delivered the detailed briefing

- 5 May 2026: The omnibus bill (record 2/3669) was submitted to the Turkish Grand National Assembly

- 14–15 and 21 May 2026: General Assembly debates and full vote

- 4 June 2026: Presidential approval and publication in the Official Gazette — now in force, with provisions applying retroactively from 1 January 2026

The practical implication for foreign IT and gaming companies is that the question is no longer “when will the package be enacted” but “how do we structure our Türkiye operation to capture the benefit”. Our earlier coverage of the package can be read in our Türkiye Yüzyılı tax package guide.

What the Türkiye Tax Reform Means for Foreign IT and Gaming Companies

The most consequential provision of the Türkiye tax reform for software and gaming exporters is the amendment to Article 10/1-(ğ) of the Corporate Tax Code: the deduction rate on qualifying service export income rises from 80% to 100%. The arithmetic is simple — effective corporate tax on qualifying revenues drops from approximately 5% to 0%.

Qualifying activities include software development, mobile games, engineering, architecture, design, call-center services, and data analysis services. To capture the benefit, four conditions must be met:

- The provider must be a Türkiye-headquartered legal entity (limited liability or joint stock company)

- Services must be invoiced to a non-resident customer abroad

- Foreign currency proceeds must be repatriated to Türkiye through the Turkish banking system

- The activity must fall within the qualifying NACE codes set out in the secondary legislation

The same package reduces the headline corporate tax rate for exporters from 20% to 14%, and to 9% for manufacturer-exporters — among the most aggressive corporate tax reductions in two decades.

Pairing the Tax Reform with Decree 10962 — Marketing Personnel Subsidy

The Türkiye tax reform is one half of the structural advantage. The other half is the marketing personnel employment subsidy under Presidential Decree No. 10962 — the consolidated services export incentive framework that has been in force since 1 January 2026.

Under the Services Sector Takeoff Program, foreign-owned Turkish entities that hire personnel for international marketing and promotion activities can claim ongoing reimbursement of personnel costs:

| Personnel Location | Monthly Salary Ceiling | Headcount Cap | Coverage Period |

|---|---|---|---|

| Domestic (Türkiye) | 90,000 TL (~USD 2,000) | 5 simultaneous | 5 years |

| Overseas (foreign branch / Star Tech Office) | 250,000 TL (~USD 5,500) | 5 simultaneous | 5 years |

The standard support rate is 50% of the eligible salary; for activities directed at designated target countries, an additional 20 percentage-point bonus brings the effective rate to 70%. Eligible roles include marketing, business development, digital product development, and overseas market promotion — the positions that directly drive international growth for IT and gaming companies.

Importantly, the personnel subsidy does not stack with most other employment incentives; only SGK premium discounts and the minimum-wage support remain compatible. For a fuller view of the supports available alongside personnel costs, see our strategic decision guide for foreign IT and gaming companies.

Combined Annual Impact — A Sample Calculation

The combined effect is easiest to see with a sample. Consider a foreign-owned Turkish entity with approximately USD 2 million in annual qualifying service export revenue and 5 domestic marketing personnel, each earning the eligible ceiling:

| Cost Item | Without Türkiye Setup | With Türkiye Entity (2026) |

|---|---|---|

| Effective corporate tax on qualifying revenue | 20–25% (typical home jurisdiction) | 0% |

| Annual tax saving on USD 2M revenue | — | ~USD 400,000–500,000 |

| 5 marketing personnel — gross annual cost | ~USD 120,000 | ~USD 120,000 |

| Reimbursement under Decree 10962 (50–70%) | — | ~USD 60,000–85,000 |

| Combined annual benefit | — | ~USD 460,000–585,000 |

The figures above are illustrative. Actual benefits depend on revenue mix, eligibility assessment, documentation quality, target country selection, and the company’s tax position in its home jurisdiction. Independent local advice is recommended for the home-side calculation.

Three Illustrative Scenarios

Important note: The three scenarios below are fictional case studies created purely to make the regulatory framework concrete. Company names and financial figures are constructed for illustration. None represents an actual Proteşvik client. USD/TRY conversions use a rate of 45.

Scenario A — DragonForge Studios (China): Mobile Gaming Studio

A 12-person mobile game studio based in Shanghai, USD 2 million annual revenue, USD 1.5 million in annual user acquisition spend. The founders establish a 100% Chinese-owned Turkish LLC and register with the Services Exporters Association (HİB). They hire 3 local marketing personnel in Ankara for UA campaign management, ASO, and growth partnerships.

- Tax saving on qualifying revenue: ~USD 400,000–500,000 annually under Law No. 7582

- Personnel subsidy on 3 local marketing hires: ~USD 36,000–50,000 annually

- Combined estimated annual benefit: ~USD 436,000–550,000

For a deeper view of the China-to-Türkiye relocation pattern, see our Türkiye relocation guide for Chinese mobile game studios.

Scenario B — DataPulse Analytics (India): SaaS Scale-up

A Series A SaaS company headquartered in Bengaluru, USD 5 million in annual recurring revenue, expanding into EU and MENA markets. The founders establish a 100% Indian-owned Turkish LLC in Istanbul. They hire 4 marketing personnel: 2 in Türkiye and 2 in their newly established Star Technology Office in Berlin.

- Tax saving: ~USD 900,000 annually under Law No. 7582

- Personnel subsidy on 2 domestic + 2 overseas hires: ~USD 80,000–120,000 annually

- Combined estimated annual benefit: ~USD 980,000–1,020,000

Scenario C — Nordlicht Studios GmbH (Germany): Casual Mobile Gaming

A Hamburg-based casual mobile gaming studio with USD 8 million in annual revenue. With an effective home corporate tax burden of approximately 30% (Körperschaftsteuer + Solidaritätszuschlag + Gewerbesteuer) and rising local talent costs, the founders evaluate establishing a 100% German-owned Turkish LLC in Istanbul and gradually shifting marketing, user acquisition, and a portion of product development to the Turkish entity. They hire 5 local marketing personnel.

- Tax saving on qualifying revenue routed through Türkiye: ~USD 1.6–2 million annually (vs. ~USD 2.4M home liability on the same revenue base)

- Personnel subsidy on 5 local hires: ~USD 60,000–85,000 annually

- Combined estimated annual benefit: ~USD 1.66–2.1 million

European studios — particularly those in Germany, Sweden, and France — face rising local talent costs and high effective corporate tax burdens. Türkiye’s geographic proximity, UTC+3 timezone, and large Turkish-speaking diaspora in DACH markets make it a natural operational complement rather than a wholesale relocation.

12-Month Activation Roadmap

For a foreign IT or gaming company moving from interest to operation, a typical roadmap looks as follows:

- Months 1–2 — Strategic Assessment: company profile, target market, and product portfolio analysis; Turkish entity structure decision (LLC for the standard case, joint stock for larger structures); office location decision

- Month 3 — Turkish Entity Setup: Turkish LLC incorporation in 1–2 weeks; minimum capital 50,000 TL (~USD 1,110); 100% foreign ownership permitted

- Months 3–4 — HİB Membership and DYS Activation: Services Exporters Association registration; Support Management System enrollment with e-signature

- Months 4–6 — Personnel Onboarding and First Applications: marketing personnel employment contracts drafted in line with Decree 10962 language; first Takeoff Program applications (Digital Product Promotion, Software Licensing, Database Membership)

- Months 6–9 — Tax Exemption Activation: NACE code alignment, invoicing structure, and foreign currency repatriation protocols established; Law No. 7582 service export exemption activated

- Months 9–12 — First Reimbursement Cycle: documented eligible expenses submitted; initial reimbursement claims under the Takeoff Program

Frequently Asked Questions

When did the Türkiye tax reform take effect?

Law No. 7582 was published in the Official Gazette No. 33270 on 4 June 2026 and is now in force. The qualifying provisions — including the Article 10/1-(ğ) amendment that brings effective corporate tax on service exports to 0% — apply retroactively from 1 January 2026.

Can a foreign company access the 0% effective tax without a Turkish entity?

No. The exemption is available only to Turkish-headquartered legal entities (LLC or joint stock company). Foreign-owned Turkish LLCs qualify — 100% foreign ownership is permitted and no Turkish co-shareholder is required.

Which positions qualify for the marketing personnel subsidy?

Decree 10962 covers personnel employed for international marketing, business development, digital product development, and overseas market promotion activities. The position title in the employment contract should align with the Ministry’s regulatory language to support the application.

How does the target country bonus work?

For activities directed at designated target countries published by the Ministry of Trade, the standard 50% support rate increases by 20 percentage points to a maximum of 70%. The target country list is updated periodically and is sector-aware.

Can a company combine the tax exemption and the personnel subsidy simultaneously?

Yes. The Article 10/1-(ğ) exemption (Law No. 7582) and the personnel subsidy (Decree 10962) operate under different legal anchors and can be claimed concurrently by the same Turkish entity, provided the qualifying conditions of each are independently met.

Is HİB membership mandatory?

Yes for the Decree 10962 supports. Services Exporters Association (HİB) membership is a prerequisite for all Takeoff Program applications, including the personnel subsidy. The tax exemption under Law No. 7582 does not depend on HİB membership but does require qualifying NACE codes and proper invoicing structure.

What is a typical reimbursement timeline?

Once a complete file is submitted through the Support Management System (DYS), reimbursements typically arrive within 3–6 months, depending on file completeness and Ministry workload. Upfront funding is not required — the framework operates on a reimbursement basis against documented eligible expenses.

How Proteşvik Helps

Proteşvik offers a complimentary 30-minute feasibility assessment for foreign game studios and IT companies considering Türkiye. The assessment covers:

- Eligibility analysis against Law No. 7582 and Decree 10962

- Indicative annual combined benefit (tax exemption + personnel subsidy)

- Strategic recommendations on Turkish entity structure and timing

- A concrete 12-month operational roadmap tailored to the company’s profile

With more than 15 years of hands-on experience in Türkiye’s incentive ecosystem, our consultants translate the Türkiye tax reform and the Decree 10962 framework into operational outcomes. For the full scope of our work, see our consultancy services overview.

Official references:

- Resmî Gazete (Official Gazette)

- Ministry of Trade — Services Sector Supports

- Support Management System (DYS)

- Invest in Türkiye (official investment agency)

See Your Türkiye Potential Before You Incorporate

A 30-minute complimentary feasibility assessment will clarify your eligibility under Law No. 7582 and Decree 10962, indicative annual combined benefit, and a concrete 12-month roadmap tailored to your company.

Request Feasibility Assessment →

📞 +90 (530) 160 10 65 | ✉️ [email protected] | 💬 WhatsApp